Makes Life Sales Easy

Whether you're positioning life insurance or a life/Roth blend, Legacy Done Right shows a clear, straight-forward analysis of the extra legacy your recommendation can generate.

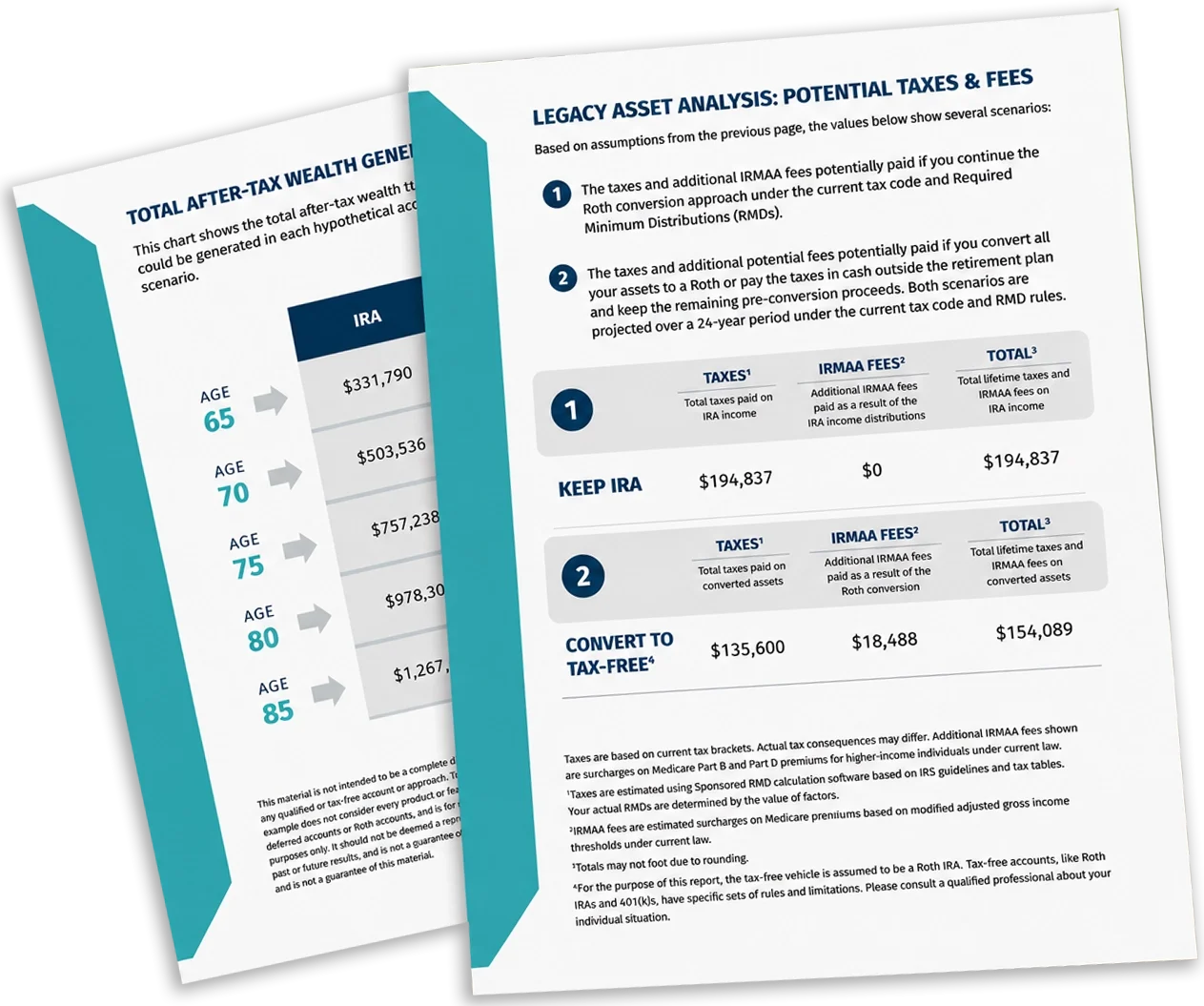

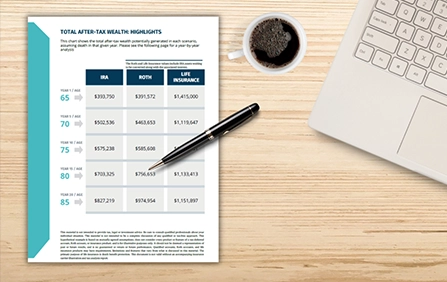

IRAs are an inefficient way to pass legacy to the next generation. With Legacy Done Right, your client gets a clear, visual report showing the value of leveraging life insurance and even Roth accounts into their legacy planning. No jargon, just numbers that matter, presented to drive informed decisions.

Enter tax assumptions and your chosen legacy structure. The software will generate a life insurance structuring guide for you, and a powerful strategy analysis for your client comparing their IRA to your recommended approach.

Whether you're positioning life insurance or a life/Roth blend, Legacy Done Right shows a clear, straight-forward analysis of the extra legacy your recommendation can generate.

Legacy Done Right helps you maximize legacy values by analyzing the best life insurance structure to drive results.

See how advisors are using Stonewood software to win larger cases and deliver better outcomes for their clients.

An advisor was working with a prospect who was a real "do-it-yourselfer" when it came to Roth conversions. The client was converting assets up their existing tax bracket – and hadn't considered any impact to IRMAA.

With Roth Done Right, the advisor was able to show an alternate pattern that sped up the conversion to 6 years. The new structure offered $30,000 savings in conversion taxes – a 20% reduction on the prospect's conversion tax bill. The report also showed hundreds of thousands of dollars in long-term tax and IRMAA savings from the converted assets – an amount the prospect hadn't been able to quantify on his own.

A new client with $1M in new AUM, and a $1M FIA sale to fund the conversion process.

An advisor was working with a prospect who already had assets with Ken Fisher. Fisher's team presented a 5% systematic withdrawal projection, so the advisor needed a stronger way to frame the income conversation.

Using the Annuity Alpha report, the advisor showed how an annuity could deliver over 8% in annual cash flow with lifetime income, plus a long-term care doubler. The contrast was clear enough that the prospect moved forward.

$1.5M placed and a $100K in new business revenue.

An advisor was working with a 58-year-old couple with an established, well-funded retirement income plan, leaving an additional $3M IRA to build out a legacy for the kids. The couple's existing advisor had no real additional plan for this money, other than to keep it in their managed account and grow that money as much as possible for the kids.

Using the Legacy Done Right report, the advisor showed the need for tax planning on this $3M IRA. According to the advisor, the simple analysis "opened up the wallet" to the Roth conversion story. The advisor then used the blended Roth/Life feature in the report to show a blend of Roth Conversion assets with some Life Insurance to help maximize the client’s legacy.

$3M in motion. The advisor picked up a $1.5M FIA sale that will be converted to Roth. And the advisor also sold a 5-Pay Protection focused IUL policy at $225,000 of premium per year.

An advisor group incorporated the Total Tax Burden report into the strategy presentation for all new prospects. They ran the tax snapshot for every new client as part of their first meeting conversation, quantifying the growing tax burden of IRA money – and illustrating the kinds of tax savings possible when working with their firm.

Starting in January of 2023, this simple analysis was presented to every single prospect who walked in the door. The goal was to differentiate their practice and drive overall revenue growth through various Roth conversion strategies.

From 2022 to 2025, new annual AUM rose from $5M to $50M. Annual FIA sales rose from $3M to $35M. And annual life premium rose from $50K to $1M.

Show your client how to reduce taxes and IRMAA - for themselves and their heirs. Legacy Done Right puts life-based legacy plans into action.

Open the tax and legacy conversation with annuity and AUM clients to increase wallet-share and deliver higher value.

Share the report with CPAs and tax attorneys to increase referrals and build confidence in your practice’s legacy approach.

Legacy Done Right is available exclusively through Stonewood’s Premium+ Membership ($329/mo). Membership includes team licenses, coordinated marketing tools, 1:1 coaching, and both live and on-demand training.

*Monthly pricing includes a one-time set-up fee of $329

Yes. Legacy Done Right allows you to compare your client’s IRA to a life insurance policy, or a blended strategy using life insurance and Roth accounts.

Absolutely. Legacy planning covers inheritance projections, gifting strategies, and beneficiary planning for clients at any wealth level. If your client has funds in an IRA or 401(k), Legacy Done Right can help.

Yes. Whether you’re recommending a limited pay, lifetime pay or alternate life insurance structure, the Legacy Done Right report will evaluate the total after-tax wealth your client can generate.

Legacy Done Right is the client-facing legacy planning software advisors use to turn an inheritance conversation into a clear, easy-to-understand report. Show a client, in plain numbers, the potential tax benefits of using life insurance to pass wealth to the next generation.

It is the report that helps a client see why how they leave money matters just as much as how much money they leave

Most legacy planning software for advisors is built to draft and store documents. Wills, trusts, powers of attorney, the legal instruments a client needs in place. That work matters, and your client’s attorney handles it.

Legacy Done Right does something different. It shows clients the most tax-efficient way to pass their legacy on to heirs, often leveraging life insurance, Roth conversions, or a blend of multiple strategies. It shows, in a clear client-facing report, how a life-insurance-based wealth transfer can change what heirs receive after taxes, so the client can make an informed decision.

Legacy Done Right answers the question: “What is the smartest way to pass this money on, and why?” That question is where the advisor adds value, and how clients can make confidence decisions.

Legacy Done Right is designed to make a wealth-transfer decision easy to evaluate and understand. The report does the explaining for you

A traditional retirement account passed to heirs can carry a tax bill that lands on the next generation. Legacy Done Right shows the after-tax value of leaving assets as they sit today versus repositioning them, so a family sees what their heirs may actually keep rather than a headline balance.

Life insurance can play a specific role in passing wealth efficiently. The software helps you show a client how a life-insurance strategy can change the after-tax amount that reaches their heirs, framed as a comparison they can follow rather than a product pitch.

Put two paths next to each other: the current plan, and a repositioned plan. The report compares what each approach may leave to the next generation, so the trade-offs are clear and the client is the one drawing the conclusion.

For clients already weighing a Roth conversion, Legacy Done Right connects the tax conversation to the legacy conversation, so a repositioning decision can be looked at for both lifetime taxes and what is left behind. It pairs naturally with the Roth Done Right side of the Stonewood suite.

The output is a clean, plain-language report built for a client meeting, with large fonts and clear charts. It moves the legacy conversation from someday to a decision.

Legacy Done Right is client-facing legacy planning software for financial advisors. You enter a client’s assets and goals, and the software produces a clear report showing the potential after-tax impact of a wealth-transfer strategy, including the tax benefits of using life insurance in legacy planning. It is built to be shown to a family during the meeting.

Enter the basics. The client’s assets earmarked for legacy, their goals for heirs, and a reasonable set of assumptions.

Choose the comparison. Look at the current plan against a repositioned, life-insurance-based approach.

Generate the report. In a few minutes you have a client-facing analysis with clear charts and plain language.

Have the conversation. Walk the family through what each path may leave to the next generation after taxes.

The hardest part of a legacy conversation is not the math, it is making the math mean something to a family sitting across the table. Legacy Done Right is built for that moment, which is why advisors treat it as a client-conversion tool rather than a back-office utility.

Legacy Done Right is part of a software suite that has run more than 114,000 client reports for over 8,000 advisors. Results vary by advisor and client situation, and the report is built to support a fair, compliant conversation rather than to promise an outcome.

Stonewood is a software and marketing platform that can be used by advisors at any IMO. We do not distribute products, participate in commission, or push you toward one carrier over another. Legacy Done Right works with any carrier, through any IMO, on your terms.

Legacy Done Right’s job is to show the family a fair comparison so they can make an informed decision, not to sell a specific policy. The recommendation stays yours; the software just makes the legacy math visible.

Legacy Done Right is an analysis tool for advisor use. It does not draft legal documents, give legal or tax or investment advice, or replace a client’s attorney or tax professional. Legacy documents such as wills and trusts should be prepared by a qualified legacy attorney, and specific tax decisions should run through the client’s qualified tax professional. Any life-insurance values shown reflect a specific illustration and are subject to the claims-paying ability of the issuer, and suitability should be evaluated against the client’s full situation and the applicable best-interest standard.

Drafting platforms and Legacy Done Right solve different problems, and many advisors use both. One produces the legal documents. The other helps the family decide what those documents should accomplish.

| Capability | Legacy Done Right | Typical drafting platform |

|---|---|---|

| Core job | Decide the wealth-transfer strategy | Draft and store documents |

| After-tax legacy comparison | Built in | Varies |

| Life-insurance tax-benefit analysis | Yes | Rare |

| Client-facing report to present live | Yes | Often document-focused |

| Drafts wills, trusts, POAs | No, by design | Yes |

| Tied to a carrier or distribution | No. | Varies |

Legacy Done Right is included in Stonewood’s Premium+ Membership, alongside Roth Done Right, Annuity Alpha, Total Tax Burden, the Retirement Tax Bill lead-gen program, and every marketing toolkit and training library. Premium+ is $329 per month, or $3,200 per year, with a one-time $329 setup fee, and every membership includes licenses for your entire team.

Most advisors want to see the report before they decide. That is exactly how we recommend starting: request a sample report, see the analysis on a real scenario, then book a short demo to watch it run live.

Legacy planning software for advisors helps a financial advisor support a client’s wealth-transfer decisions. Some tools draft legal documents like wills and trusts. Legacy Done Right is a client-facing analysis tool that shows the potential after-tax impact of a wealth-transfer strategy, including the tax benefits of using life insurance in legacy planning.

No. Legacy Done Right is an analysis and conversation tool, not a document-drafting platform. It helps a family decide what their legacy strategy should accomplish, and a qualified legacy attorney prepares the legal documents. Many advisors use Legacy Done Right alongside a separate drafting solution.

It compares wealth-transfer paths side by side, showing what a current plan versus a repositioned plan may leave to the next generation after taxes. The goal is to make the trade-offs clear so the client can make an informed decision, with the advisor guiding the conversation.

Yes. Legacy Done Right is built to be shown to a family during the meeting, with large fonts, clear charts, and plain language.

Life insurance can play a role in passing wealth efficiently. Legacy Done Right shows a client how a life-insurance strategy may change the after-tax amount that reaches their heirs, framed as a fair comparison rather than a product pitch. Death benefit value is used from a specific carrier illustration and is subject to the claims-paying ability of the issuer.

Legacy Done Right is included in Stonewood’s Premium+ Membership at $329 per month, or $3,200 per year, plus a one-time $329 setup fee. Every membership includes licenses for your whole team, along with the rest of the Stonewood software suite and training.

No. Stonewood is a software and marketing platform that can be used by advisors at any IMO. We do not distribute products, participate in commission, or push you toward one carrier over another. Roth Done Right works with any carrier, through any IMO, on your terms.

The fastest way to understand Legacy Done Right is to see a real scenario. Request a sample report, then schedule a short demo and watch it run live.